Making Accounting AI | White Paper

How Artificial Intelligence Will Reshape the Accounting Profession. And Why Waiting Is No Longer an Option

By Daniel Lawrence, Founder, bots for that | Enterprise Automation & AI Specialist | Thought Leader in AI for Professional Services

“The question is no longer whether AI will transform accounting. The question is whether accountants will lead that transformation, or be replaced by it.”

Foreword: A Different Perspective

Most white papers on AI in accounting are written by people who came from accounting. They understand the profession deeply, but they understand AI the way most of the sector does, as something new, exciting, and slightly uncomfortable.

I come from a different place.

I’ve spent well over a decade deploying enterprise-grade automation and artificial intelligence in some of the most complex, regulated, and high-stakes environments imaginable. Financial services. Healthcare. Critical infrastructure. Large enterprises where the margin for error is zero and the volume of data is enormous. Environments where AI isn’t a feature, it’s load-bearing.

A few years ago, I turned my attention to the profession where it all began for me, accounting.

What I found was a profession of genuinely talented, hard-working people, sitting on top of a mountain of structured, recurring, predictable, high-value data, doing an enormous amount of work by hand. To put it simply, it hadn’t changed that much from when I started nearly three decades earlier.

And I thought: this is the most automatable profession I’ve seen.

This paper is written from that vantage point. Not from inside the profession, but from outside it, with deep respect for what accountants do, and with urgent concern about what happens next if the profession doesn’t act.

Part One: The Burning Platform

1.1 Accounting Has Always Been a Data Business

Accounting is, at its core, an information profession. It is the systematic capture, classification, reconciliation, and communication of financial data. Every single one of those words (capture, classify, reconcile, communicate) describes something that artificial intelligence is exceptionally good at.

This isn’t a coincidence. It’s an opportunity.

The accounting profession has historically been insulated from technology disruption by complexity, regulation, and the trust that clients place in their advisors. Those protections still exist. But they are thinning, and faster than most practitioners realise.

1.2 The Numbers Don’t Lie

- The British Chambers of Commerce, in partnership with Intuit, found that 35% of UK SMEs were actively using AI in 2025, up from just 25% in 2024. A more recent BCC/University of Essex report puts that figure at 54% of UK firms now using AI in some form.

- Yet despite that headline growth, only 11% of UK SMEs report using technology to a “great extent” to automate or streamline their operations. The majority are dabbling, 42% “to some extent,” 29% minimally. (British Chambers of Commerce / Intuit, September 2025)

- A March 2026 survey of 1,000 UK SME leaders by Paragon Bank found that half now say they’re likely to replace some staff roles with AI. Yet only 1 in 10 has built the operational foundation to do it.

- The Wolters Kluwer Future Ready Accountant report (2025, 2,700+ professionals globally) found that AI adoption among accounting firms more than quadrupled in a single year, from 9% in 2024 to 41% in 2025, with 77% of firms planning to increase AI investment further.

- Karbon’s State of AI in Accounting report identified what it calls “the AI paradox”: 82% of accountants are intrigued or excited by AI, yet only 25% are actively investing in AI training for their teams.

That gap between intent and capability is the most important number in this paper. Half of your clients are already planning to reduce their reliance on human roles. Barely one in ten has the infrastructure to act on it yet. That window, between intent and execution, is where the accountant’s opportunity lives. But it will not stay open indefinitely.

1.3 The Client Is Already Moving

Your clients are not waiting for you to recommend AI. They’re finding it themselves.

Tools like ChatGPT, Copilot, Gemini, and a growing list of specialist fintech applications are being adopted by business owners right now, often quietly, often without their accountant’s knowledge. They’re using them to draft board reports, interpret management accounts, query VAT returns, chase debtors, and increasingly, to ask questions that used to require a phone call to you.

When a client stops calling, it doesn’t always mean they’re happy. Sometimes it means they’ve found an alternative.

Part Two: The AI Landscape — What's Real and What Isn't

The term “AI” is doing a lot of heavy lifting right now. And the accounting software market is one of the worst offenders.

Over the past two to three years, almost every major accounting platform has announced “AI features.” Auto-categorisation of transactions. Suggested reconciliation matches. Smart inbox management. Predictive cash flow. (and yes, yours truly and the good folks here at Bots For That, were among them, the irony isn’t lost on me.)

These are useful features. They represent incremental improvement. But let’s be honest about what they are: workflow enhancements built on pattern matching and rules engines. Some of them don’t involve machine learning at all. They are dressed in the language of AI because AI is what the market wants to hear.

This matters, because it creates a false sense of progress.

Firms that adopt these tools check the “AI” box internally and move on. They believe they’re at the frontier. They’re not. They’ve taken one step in a ten-step journey, and they’ve mistaken it for the finish line.

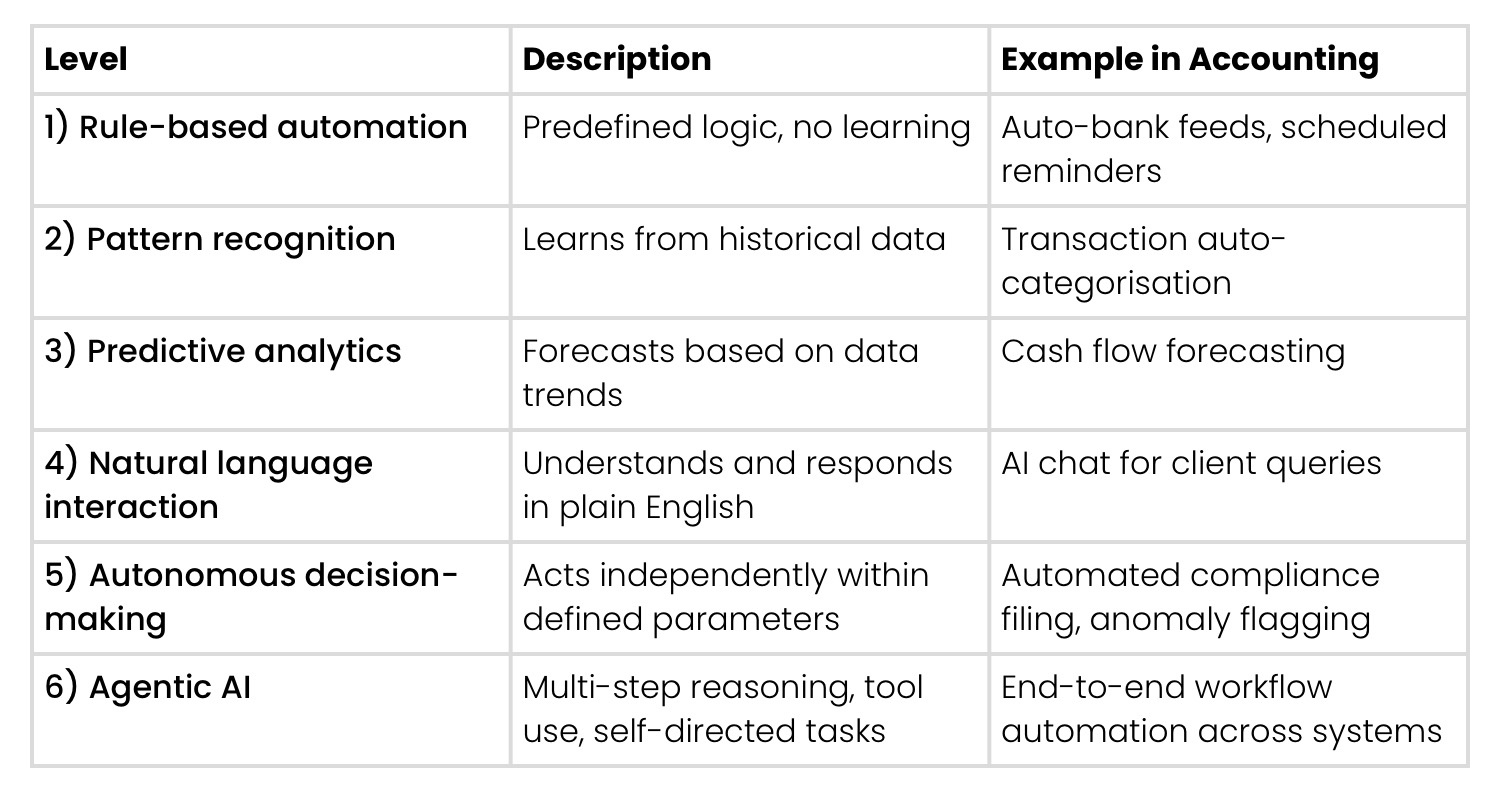

2.2 The Spectrum of AI Maturity

To understand where the profession needs to go, it helps to understand where AI actually sits on a maturity curve:

Most accounting software sits firmly at Levels 1–2. The most advanced specialist tools are reaching Levels 3–4. Levels 5 and 6, where the real transformation happens, are largely untouched in this sector.

The rest of the enterprise world? In reality, it’s quite diverse, but in my experience we’ve been supporting clients in other sectors to operate at Levels 4, 5, and 6 for a while.

The accounting profession is not behind by months. It is behind by years.

2.3 Why “AI-Wrapped” Products Are Not the Answer

There is a category of product, growing rapidly, that deserves particular scrutiny. These are tools that place a conversational or generative AI interface on top of existing functionality. You type a question; the tool queries its database; the answer comes back in natural language.

This is fine as far as it goes. But it is not transformation. It is the same process with a friendlier front door. The most apt name I’ve heard used for this, is “super-google”.

The accounting profession’s tendency to adopt these tools and call it “AI implementation” is understandable, they’re safe, familiar, and endorsed by the platforms that firms already trust. But they don’t change the underlying workflow. They don’t eliminate the manual work. They don’t free up the advisor’s time in any meaningful way. And they don’t future-proof the practice.

They are, in many cases, a very effective way of feeling like you’re doing something, while doing very little.

2.4 Agentic AI and AI Agents — Cutting Through the Hype

No term in the current AI conversation is more overused, more misunderstood, or more commercially exploited than “AI agents” and “agentic AI”. Let me be precise, because precision matters enormously here.

What agentic AI actually means:

An AI agent is a system that can perceive its environment, make decisions, take actions, and, critically, adapt based on the outcomes of those actions. True agency means the system can plan across multiple steps, use tools and external systems, handle unexpected situations, and pursue a goal without a human directing every move.

A genuinely agentic system operating in accounting might: receive an alert that a client’s VAT return is approaching, retrieve the relevant transaction data from the accounting platform, identify and flag anomalies for human review, prepare a draft return, notify the responsible accountant with a summary of anything requiring judgement, and, once approved, go ahead and submit directly to HMRC. All without being prompted.

What most “AI agents” in accounting actually are:

A pop-up chat window. A workflow that runs three steps and calls it a pipeline. A button that triggers a predefined macro and returns the result in conversational language.

These are not agents. They are scripts with better presentation and marketing.

The distinction is not academic. If you invest in a platform on the promise of “AI agents” and what you get is a slightly faster version of your existing process, you haven’t automated your practice, you’ve redecorated it.

The questions to ask any vendor claiming agentic AI:

- What decisions does the system make autonomously, and what are its decision boundaries?

- How does it handle situations it hasn’t encountered before?

- What tools and external systems can it interact with natively?

- Can you show me a multi-step workflow that runs end-to-end without human intervention?

- What does the audit trail of an agent’s decision-making look like?

If the answers are vague, the “agentic AI” is almost certainly a polished automation script.

True agentic AI is coming to accounting. It will be transformative. But the firms that invest in the real thing, built on genuine AI infrastructure, by teams that have deployed agents at scale, will be in a categorically different position to those who bought the marketing.

Part Three: The Profession in the Mirror

3.1 Good Intentions, Insufficient Action

Let me be direct, because I think the profession deserves directness more than it deserves another carefully hedged report.

The accounting sector, by and large, wants to embrace AI. In survey after survey, practitioners express genuine interest, genuine curiosity, even genuine enthusiasm. The intention is there.

But intention without action is just aspiration.

What typically happens is this: a firm identifies AI as a strategic priority. They form a working group, or appoint a “digital champion.” They attend a webinar or two. They read a white paper, perhaps even this one. And then they wait. They wait for the technology to mature. They wait for their software vendor to build it in. They wait for a competitor to go first and prove it works. They wait for the perfect conditions. This is the comfortable home of the laggard.

The perfect conditions don’t come.

3.2 The Paralysis of Perfectionism

This waiting behaviour is not unique to accounting. I’ve seen it in every industry I’ve worked in. It goes by different names, risk management, due diligence, strategic patience, but it all amounts to the same thing: a preference for the known over the unknown, even when the known is clearly no longer sustainable.

What makes it particularly dangerous in accounting is the regulatory environment. Practitioners are conditioned to avoid error. Compliance means precision. And precision, in many minds, means manual oversight. The idea of delegating judgment to a system, even a well-designed, well-tested one, feels opposed to professional standards.

But here’s the reframe: the manual process is not the safe option anymore. Human error in high-volume, time-pressured compliance work is not a theoretical risk, it is a daily reality. The risk of not automating is now greater than the risk of automating thoughtfully.

3.3 The “Safe Choice” That Isn’t Safe

When accounting firms do act, they tend to converge on the same options: add the AI features in their existing platform, perhaps add a second-tier tool with a recognisable brand. They choose what feels safe, familiar, and low-risk.

I understand the logic. I don’t agree with the conclusion.

The firms that will lead this profession over the next decade are not going to be the ones who waited for their existing vendor to catch up. They’re going to be the ones who looked beyond the familiar, asked harder questions, and chose tools built specifically for the problems they were trying to solve.

In every other industry where I’ve worked, financial services, betting and gaming, healthcare, logistics, the firms that transformed were the ones that went to specialists. Not the generalist platform with a new AI tab. The specialist.

This is not a coincidence. And it is not going to be different in accounting.

The term “AI” is doing a lot of heavy lifting right now. And the accounting software market is one of the worst offenders.

Over the past two to three years, almost every major accounting platform has announced “AI features.” Auto-categorisation of transactions. Suggested reconciliation matches. Smart inbox management. Predictive cash flow. (and yes, yours truly and the good folks here at Bots For That, were among them, the irony isn’t lost on me.)

These are useful features. They represent incremental improvement. But let’s be honest about what they are: workflow enhancements built on pattern matching and rules engines. Some of them don’t involve machine learning at all. They are dressed in the language of AI because AI is what the market wants to hear.

This matters, because it creates a false sense of progress.

Firms that adopt these tools check the “AI” box internally and move on. They believe they’re at the frontier. They’re not. They’ve taken one step in a ten-step journey, and they’ve mistaken it for the finish line.

Part Four: The Existential Question

4.1 The Threat Nobody Wants to Say Out Loud

Let me ask the question that a lot of people in this industry are thinking but not saying.

If a business owner can open ChatGPT and ask (and get a credible answer in thirty seconds): “I’ve attached my last three months of bank statements, can you categorise these transactions, flag any anomalies, and tell me what my rough tax position is?”

What is the value proposition of the accountant?

This is not a rhetorical attack on the profession. It is the most important question accountants need to be able to answer. And right now, too many can’t answer it clearly.

4.2 The Democratisation of Financial Intelligence

Five years ago, the tools required to perform meaningful financial analysis were expensive, specialised, and required expertise to operate. That expertise, in software, in data, in interpretation, was part of what an accountant sold.

That no longer holds true.

AI has democratised access to financial intelligence at a speed that is still accelerating. The barrier to entry for a business owner who wants insight into their own finances has dropped from “hire a professional” to “ask a question”.

The category of work that accountants used to be paid for, data gathering, transaction processing, basic reporting, is being automated away. Not slowly. Now. And in case you hadn’t connected the dots yet, one very stealthy example of this, is our old friend MTD.

4.3 The Advisory Gap — and the Opportunity Inside It

Here’s the important counterpoint.

What AI cannot do, not yet, and not without significant human oversight, is provide the contextual, relationship-based, strategically-informed advice that comes from knowing a client’s business, their goals, their risk appetite, their history. AI can tell you what the numbers say. It cannot tell you what they mean for this business, this owner, in this moment in time.

That gap is the accountant’s future.

But, and this is the critical point, accountants can only occupy that gap if they’re not still buried in the work that AI is replacing. If the firm’s capacity is consumed by data entry, reconciliation, chasing missing information, and churning out compliance outputs manually, there is no space to become the advisor the client actually needs.

The automation of compliance work is not a threat to accountants. It is the prerequisite for their next chapter.

4.4 Nobody Is Coming to Rescue You

This needs to be said plainly.

The major accounting software vendors are not going to solve this for you. They are building features to retain market share, not to transform your practice model. The professional bodies are not going to get ahead of this curve. They are inherently conservative institutions that reflect consensus, not anticipate it.

Your clients are not going to wait. They are already exploring alternatives.

And the AI tools that could replace the routine work accountants do today cost less per month than a tank of petrol.

The window for proactive transformation is open right now. It will not stay open indefinitely. The firms that move in the next twelve to eighteen months will define the next generation of accounting. The firms that wait will find themselves competing for a smaller and smaller piece of a market that has already moved on.

There is no cavalry. There is no safety net. There is only the decision in front of you.

Part Five: The Path Forward

5.1 What “Good” Looks Like

Across the industries where I’ve built AI-powered operations, the firms that got it right shared a common pattern. They didn’t try to automate everything at once. They started with a clear purpose, and the highest-volume, most repetitive, most clearly-defined workflows. They proved value fast, built confidence, and expanded from there.

In accounting, the equivalent is clear:

Phase 1 — Compliance Automation. Automate the routine. Client data ingestion, transaction processing, VAT return preparation, payroll reconciliation, deadline management. These are well-defined, high-volume, rules-based tasks. They are the ideal entry point for AI (and contemporary automation). The goal is not to remove the accountant, it is to remove the accountant from work that does not require their judgment.

Phase 2 — Portfolio Intelligence. Deploy tools that give firms real-time visibility across their entire client base. Not client-by-client, not system-by-system, but portfolio-wide. Which clients have anomalies in their accounts? Which ones are approaching a cash crisis? Which businesses show signs of growth that the accountant should be having a conversation about? This is where AI turns data into advisory opportunity.

Phase 3 — Client-Facing AI. Build AI-powered touchpoints into the client relationship. Automated reporting. Conversational interfaces for routine queries. Proactive alerts. The goal is not to reduce the relationship, it is to increase the frequency and quality of meaningful contact while reducing the friction of routine interaction.

Phase 4 — The Advisory Practice. With the first three phases in place, the firm has capacity. Capacity to have conversations that generate real value. Capacity to offer strategic advisory services. Capacity to price on impact rather than hours. This is the destination, a practice model that is genuinely defensible in an AI-native world.

5.2 The Questions Every Firm Should Be Asking Now

- What percentage of my team’s time is spent on tasks that could be automated with current technology? If you haven’t done this analysis, start here. The number will be uncomfortable.

- What is the cost of that time, in salary, in opportunity, in client experience? Convert the percentage to pounds. That is the size of the problem and the size of the opportunity.

- What would my firm look like if that time were freed up? Don’t answer this with “we’d be more efficient.” Answer it with specifics: what new services could you offer? What conversations could you have? What clients could you take on? What factor could you grow by without increasing heads or costs?

- What is my current AI strategy, and is it a real strategy or a wish list? There is a significant difference between “we’re keeping an eye on AI” or “we’re using some tools” and “we have a twelve-month roadmap with named owners and specific milestones”.

- Who in my market is already doing this? Because they exist. And they are winning clients, growing, and scaling. And they’re potentially also acquiring those who aren’t, for a bargain.

5.3 A Word on Trust and Risk

The most common objection to AI adoption in accounting is trust. Can we trust the outputs? What if it gets something wrong? What about professional liability?

These are legitimate questions. They deserve proper answers, not dismissal.

The answer to trust is not to avoid AI. The answer to trust is governance. Every AI tool worth deploying comes with the ability to define parameters, set thresholds, install guardrails, require human review at defined checkpoints, and create full audit trails. The question is not whether AI can be trusted in principle, it is whether this implementation, with these controls, in this context, is trustworthy.

That is an engineering question and a process design question. It is answerable.

The firms that will never trust AI are the same firms that once resisted cloud accounting on the grounds that their clients’ data shouldn’t be “somewhere on the internet”. That argument lost. This one will too.

Part Six: Why bots for that Is Different

6.1 Built for This. Not Retrofitted to It.

There is an important distinction in this market that rarely gets made explicit.

Most AI tools in the accounting sector come from one of two places: accounting software vendors who are adding AI features to existing platforms, or fintech startups that were born in accounting and are learning AI as they go.

Both of these approaches share the same limitation: they are building AI understanding on top of accounting knowledge.

bots for that was built the other way around.

We are an enterprise automation and AI company that has brought over a decade-plus of hard-won expertise, from some of the most complex, regulated environments in the world, into the accounting sector.

We understand automation and AI deeply because we have been building it, deploying it, and refining it in production environments long before it was fashionable. We understand compliance deeply because we have operated in regulated sectors where the cost of error is measured in regulatory sanctions and reputational damage, not just a client complaint.

When we built MTD Command Centre, we didn’t start from “how do we build a tax tool and add some AI?” We started from “what does a genuinely AI-native, integrated compliance platform look like?” and then we worked with tax experts and built that.

6.2 What That Means in Practice

It means our architecture is built for AI from the ground up, not retrofitted. It means our integrations are built on proper AI connectivity, not screen-scraping and workarounds. It means our understanding of automation isn’t theoretical, it comes from real deployments at scale, under pressure, in regulated environments.

And it means that when we talk about AI, including agentic AI, we are talking about actual AI. Not a marketing label on a rules engine. Not a chat interface wrapped around a database. The real thing, built by people who’ve been doing it for a very long time.

6.3 bots for that’s beanieverse: A Platform, Not a Product

The beanieverse is designed as an AI-native automated accounting ecosystem – a suite of interconnected tools that each address a distinct workflow challenge in the accounting practice, and that together create something more powerful than the sum of their parts: a genuinely intelligent, genuinely integrated operating environment for the modern accounting firm.

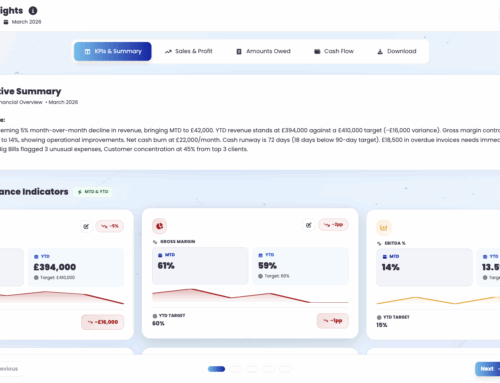

MTD Command Centre, our current most popular product, provides portfolio-wide, real-time visibility across client tax positions, compliance status, liabilities, and deadlines across Income Tax, VAT, and Corporation Tax. All powered by live HMRC data. With AI-native suggested next steps and executable actions. With “human-in-the-loop” for comforting confidence.

That is not a feature. That is a new way of running a practice.

Conclusion: The Moment Demands a Decision

The accounting profession stands at an inflection point that comes along perhaps once in a professional lifetime.

The tools to transform are available. The data environment, accelerated by Making Tax Digital, is falling in to place. The market is moving. The clients are moving. The technology is moving.

The only variable is the decision made by the accountant reading this.

There is a version of this story where the profession seizes this moment, where accountants use AI to eliminate the work that doesn’t need them, and in doing so, become the strategic partners that businesses genuinely need. Where the profession emerges from this transformation more valued, more trusted, and more indispensable than ever.

And there is another version, where the hesitation continues, the “safe” options are chosen, and the space that accountants occupied is quietly, steadily, filled by tools that don’t charge hourly rates and don’t take holidays.

Both versions are plausible. Only one is inevitable, and which one it is depends on decisions being made right now, in firms like yours.

The question is not whether to act. The question is how quickly, and how boldly.

About The Author

Daniel Lawrence is the Co-Founder of bots for that (BFT) and creator of their beanieverse, an AI-native automated accounting platform. With over a decade of experience designing and deploying enterprise automation and AI systems across financial various sectors and highly regulated industries, Daniel brings a perspective to accounting AI that is rooted in operational reality rather than vendor marketing.

He is a vocal advocate for the accounting profession’s transformation and a forthright critic of the AI-washing that characterises too much of the current market conversation.

bots for that | botsforthat.com | Enterprise AI. Built for Accounting.

Making Accounting AI is the first in a series of thought leadership publications from bots for that. The full series, AI readiness, the advisory practice of the future, agentic AI in accounting, AI governance, and building the AI-enabled firm is available at botsforthat.com.

© 2026 Bots For That LTD. All rights reserved. This white paper is provided for educational and informational purposes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}